Merchant Onboarding

May 8, 2025

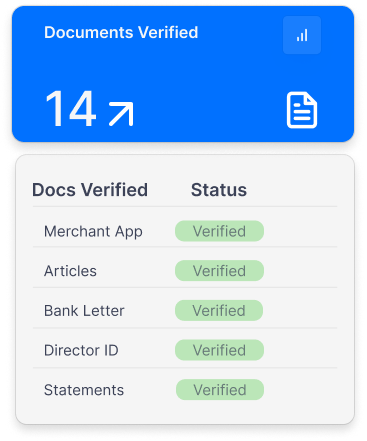

You Didn’t Automate It, You Digitized a PDF

Many payment providers merely digitize paperwork, leaving manual reviews intact. True automation uses real‑time data, AI risk signals, and seamless workflows, accelerating onboarding, reducing costs, and boosting merchant activation.

.png)